The new Government’s first Budget is set to be delivered on 30 May 2024. There has been much commentary around what the state of the nation’s finances will look like, with plenty of discussion on how the Government will fund the personal tax bracket changes that were promised by the National party during the election campaign. As a result, it is likely that tax will be a key headline for Budget 2024. Outside the personal tax bracket changes, however, there is minimal expectation of more significant tax changes being announced.

While we are not expecting any significant changes to New Zealand’s tax system in this year’s Budget, the reality is that tax will remain a key discussion point, particularly in the lead up to the next election, given the Labour party has already indicated that tax is back on the table.

In this Tax Tips, we consider the current state of the New Zealand tax system and look ahead to the key issues that are relevant in considering the health of the New Zealand tax system going forward.

Current state of the New Zealand tax system

The broad structure of the New Zealand tax system has largely remained unchanged since the significant tax reforms of the mid-1980s. The changes resulted in the broadening of the New Zealand tax base, including the introduction of goods and services tax and fringe benefits tax, and the removal of a number of incentives for businesses.

These changes allowed for a significant reduction of income tax rates, initially from 66% to 48% for the highest income earners, and a reduction of company tax rates from 45% for resident companies and 50% for non-resident companies, to 33% for all companies.

Since then, New Zealand continues to operate this “broad-base low rate” (BBLR) tax system. This system has generally delivered well for New Zealand to date, and this has been confirmed by a number of tax reviews that have been conducted over the years, with the last one being the Tax Working Group (TWG) review which was completed in 2019.1 This is largely from a perspective of whether the tax system delivers the tax revenue needed in a way that meets established principles of tax policy design.

However, the 2019 review did highlight that the current system is reliant on a relatively narrow range of taxes (being income tax) and is not particularly progressive. The taxation of capital income was also called out as an area that should be extended. The previous Government commissioned work to attempt to provide an evidentiary basis to measure the progressivity of New Zealand’s tax system. Inland Revenue’s High-Wealth Individuals (HWI) Research Project Report suggested that the median HWI family paid 8.9% of their economic income in tax.2

While ultimately the amount of tax revenue required by a country will depend on the level of spending and appetite to borrow, it is nevertheless useful to see how New Zealand is tracking compared to other developed economies. A useful measure in this context is how New Zealand compares to other OECD countries in terms of tax-to-GDP. Over the last decade, New Zealand has largely tracked close to or below the OECD average. For 2022, New Zealand had a tax-to-GDP ratio of 33.8% compared with the OECD average of 34%.3 This suggests that the amount of tax revenue collected by the New Zealand tax system is not overly out of kilter amongst OECD countries.

1 The Tax Working= Group, https://taxworkinggroup.govt.nz/index.html.

2 Although there were valid criticisms made at the time of the approach to data collection and methodology.

3 https://www.oecd.org/tax/revenue-statistics-new-zealand.pdf

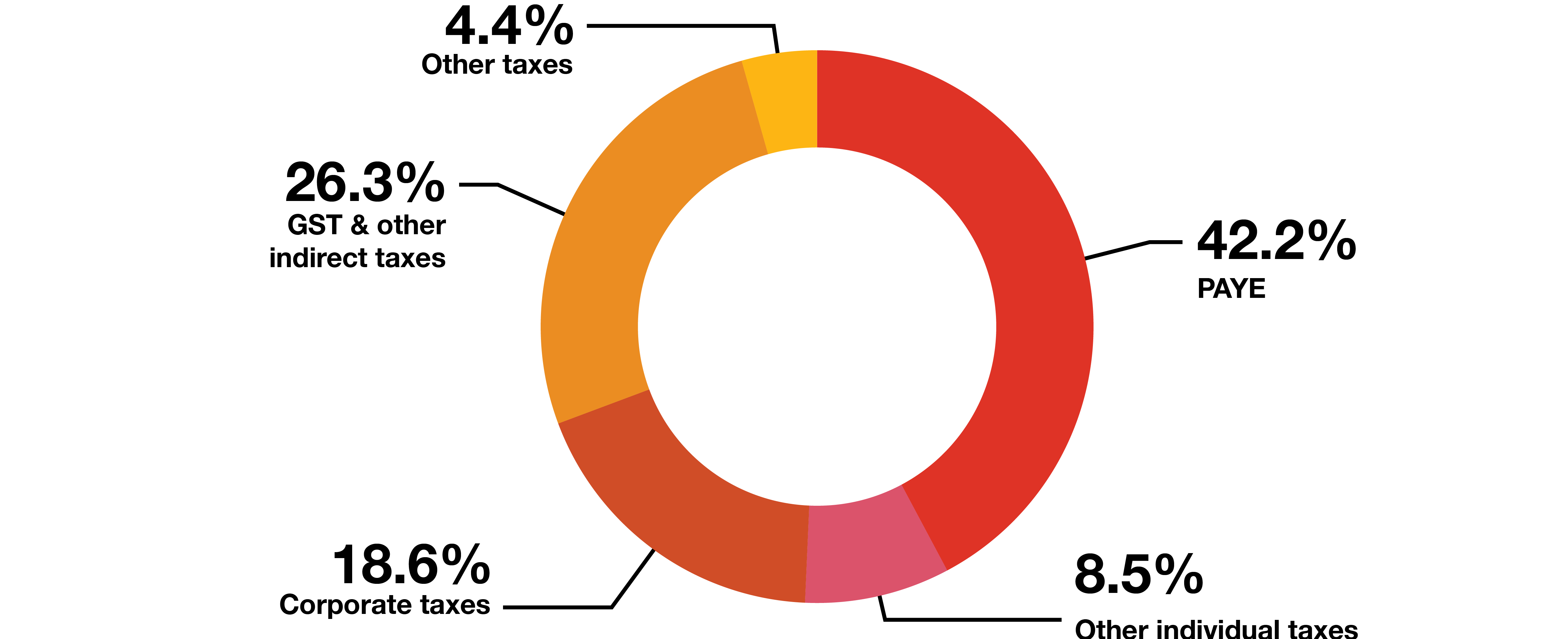

The final aspect of the current state of the New Zealand tax system that should be noted is where the tax revenue is coming from. This picks up on one of the findings from the 2019 TWG review that New Zealand is reliant on a relatively narrow range of taxes. Data shows that New Zealand is heavily reliant on taxes from individuals and most of it is from PAYE which indicates a strong reliance on tax on labour (GST as a consumption tax is also arguably a tax on labour, based on economic theory).

Tax revenue breakdown 2020-2023

Average PAYE vs Other tax revenue 2020-2023

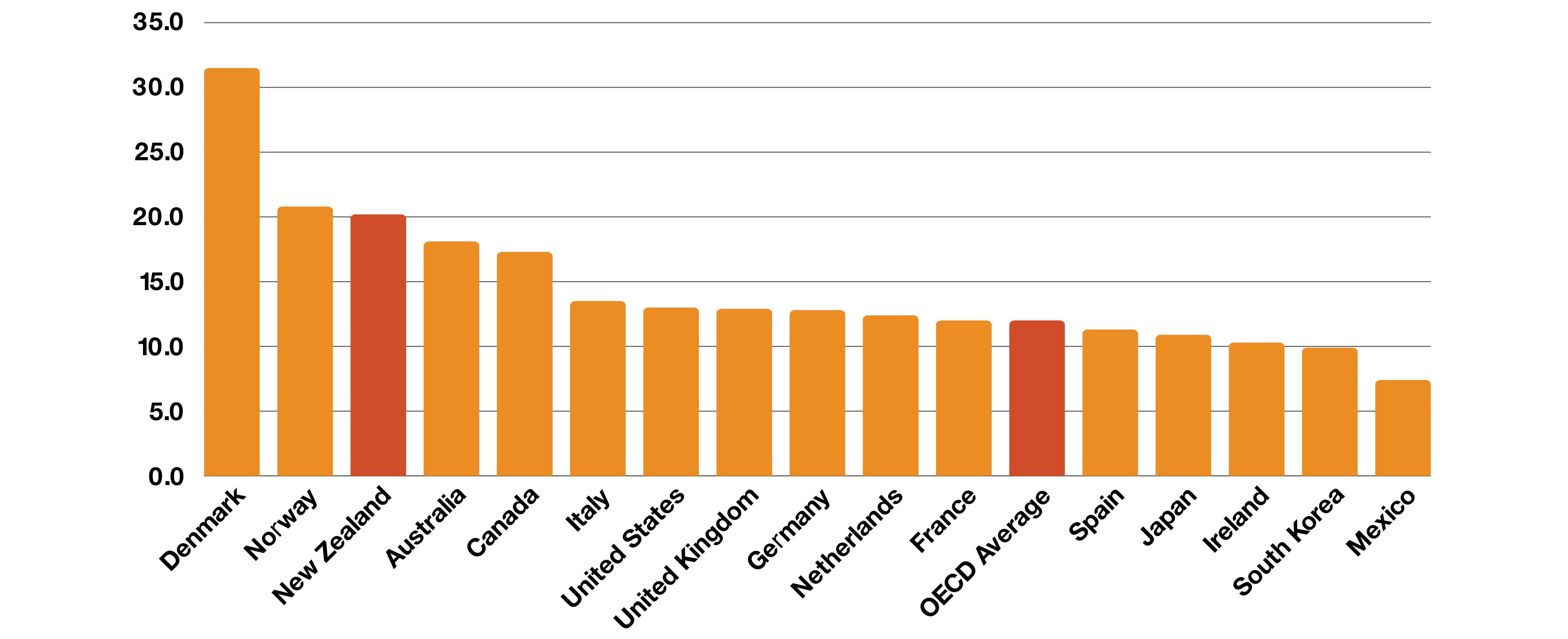

Further, as illustrated below, the proportion of New Zealand’s tax revenue that relates to income taxes (taxes on income and profits) is higher than other developed countries - indicating that New Zealand could be disproportionately reliant on income taxes.

Taxes on income and profits of OECD countries as a percentage of GDP

Future outlook for the New Zealand tax system

While the current system is seen to be performing well to generate the tax revenue necessary for New Zealand over the last 40 years, it does not necessarily mean that maintaining the status quo will continue to ensure this remains the case.

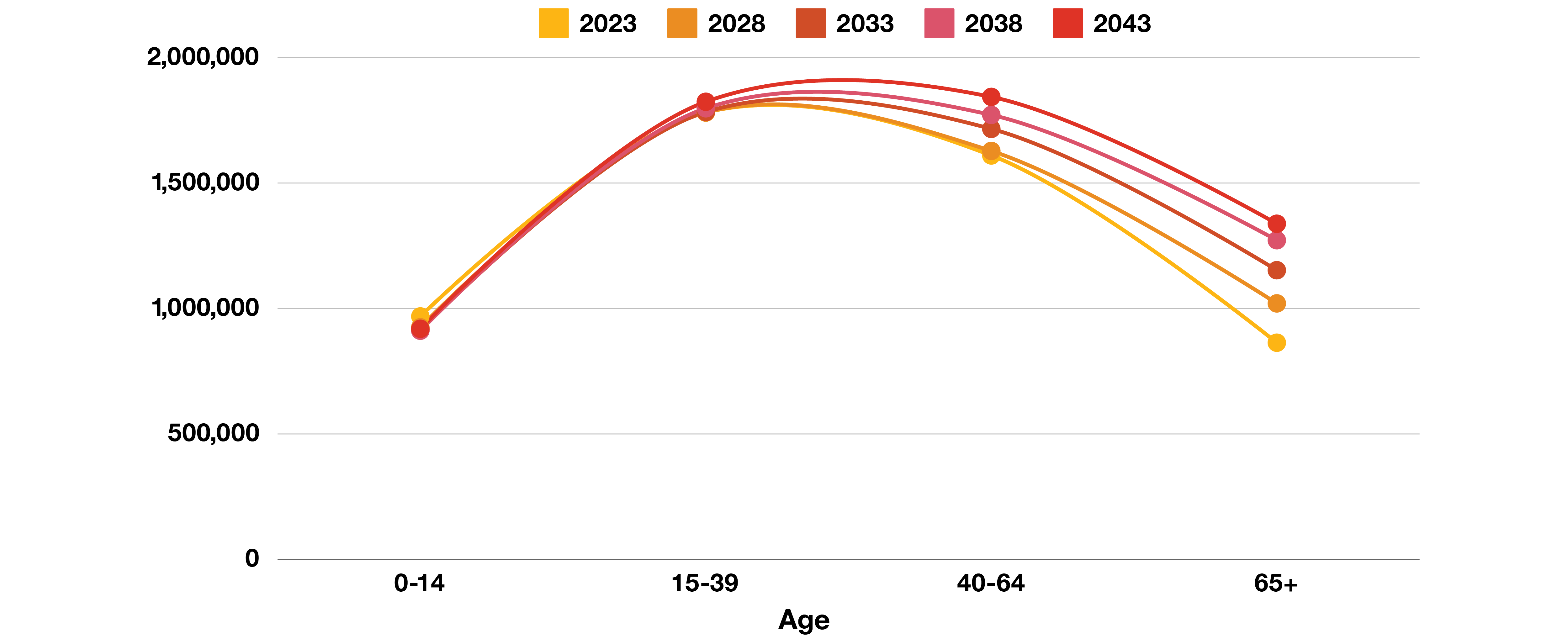

Key developments such as the changing demographics of New Zealand and technological change (e.g. the impact of Artificial Intelligence) will be important to consider given the current heavy reliance on tax on labour. As we look ahead, the assumption is that the proportion of New Zealanders working will be smaller as we grapple with an ageing population. With a lower proportion of people working, the amount of tax collected could stay static, in the absence of a change in tax rates. This may create issues as the ageing population will likely increase expenditure needs, for example health care, New Zealand superannuation, etc. assuming there are no significant policy changes.

National population age distribution 2023-2043

For completeness, there will be a number of other factors that could impact on the amount of tax revenue generated by the tax system, for example general economic conditions, or the competitiveness of the New Zealand economy and migration (which could in turn be impacted by the design of the tax system). However, the impact of these factors is arguably less stark when compared to demographic changes.

In the absence of the ability to find additional tax revenue from the existing tax base (or by growing the tax base through economic growth), the other non-tax options are to reduce government spending or borrowing to fund any shortfall. The former may require significant policy changes in a number of areas and with the latter, the Government will still have to repay the debt at some point in the future which will come back to the need to generate sufficient tax revenue.

Ultimately, looking ahead, in the absence of significant policy changes, be it tax or otherwise, it is likely that the tax system will be placed under more pressure to deliver the revenue required by the government to fund its expenditure. Overall, it may be difficult for the ecosystem to remain static if the desire is for the Government to provide a similar level of support to New Zealanders.

What are the options for change?

Setting aside non-tax policy changes which may reduce revenue needs, tax levers may be pulled to look for additional tax revenue.

Increase tax rates?

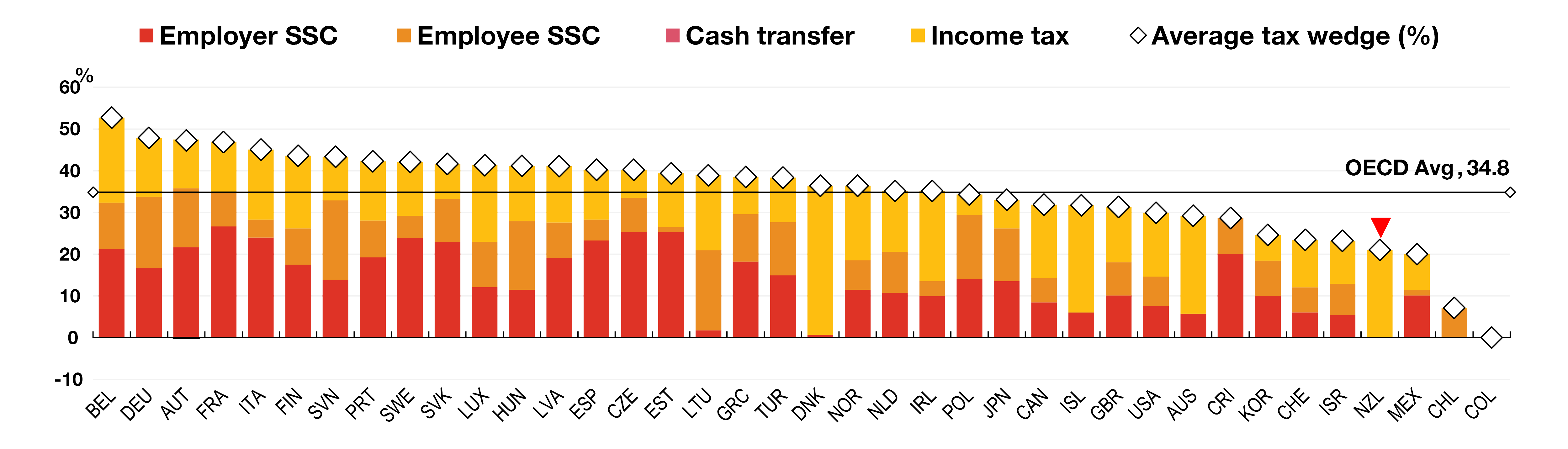

An obvious one may be to increase the amount of tax being levied on the existing base, whether it be increasing the income tax rates or GST. The OECD compares the “tax wedge” on labour income, being the amount of tax paid by both the employee and employer, and it consistently has New Zealand as having one of the lowest tax wedges among OECD countries (35th out of 38 OECD member countries). In 2023 it was 21.1%, compared to the OECD average of 34.8%.4 While at first glance, this may suggest room to lift income tax rates, it is important to note that the measure includes social security contributions, of which New Zealand has none.

Average tax wedge: average single worker, no children

A more useful comparison perhaps is looking at the employee net average tax rate which is a measure of the net tax on labour income paid directly by the employee. On this measure, New Zealand still ranks at the lower end (28th out of 38 OECD countries), but the net average tax rate of 21.1% is closer to the OECD average of 24.9% for 2023.

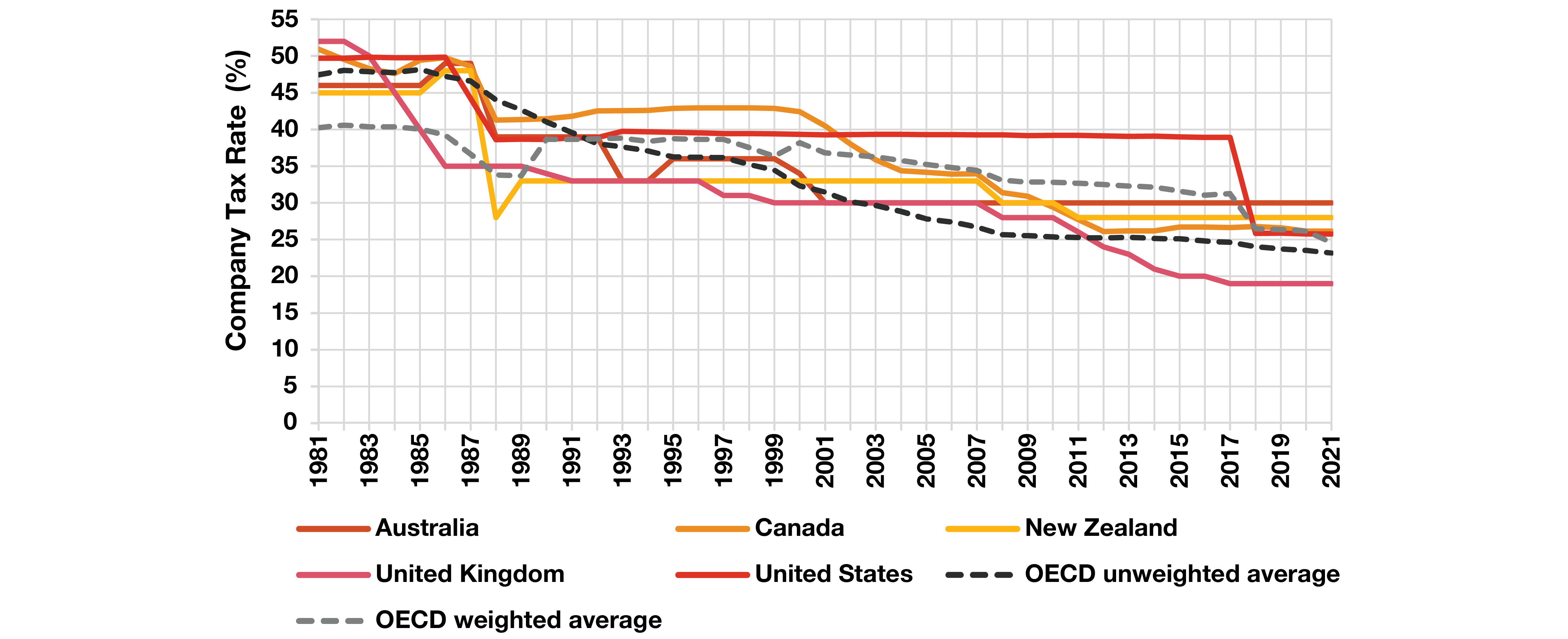

As demonstrated by the recent experience of adding a top marginal tax rate of 39%, increasing personal tax rates and thresholds could result in other issues arising from the misalignment of tax rates between individuals, companies, and trusts. These issues become more pronounced as the gap between personal income tax rates and company / trustee tax rates becomes greater, and globally there is a trend towards lower corporate tax rates (although this trend has slowed down recently as governments struggle with the fiscal impact of Covid-related spending).

FIgure 1.1: Company tax rates in NZ and some othe OECD countries

Source: Inland Revenue Long Term Insights Briefing 2022

New Zealand has a relatively low GST rate compared to other OECD countries (averaging 19.2% as of 31 December 2022). However, this is against the context of a very broad GST base in New Zealand when compared to other countries.

4 https://www.oecd.org/tax/tax-policy/taxing-wages-new-zealand.pdf

New taxes?

Another option is to broaden the tax base further, in effect taxing things that currently sit outside the existing tax system. A number of options have been the topic of discussion over the last few years, in particular leading up to the 2023 general election, and include the introduction of a comprehensive capital gains tax or a wealth tax.

With any tax policy changes, they are often assessed against the well established tax policy design principles, namely:

Efficiency

Equity and fairness

Revenue integrity

Fiscal adequacy

Compliance and administration costs

Coherence

It is worthwhile noting that there will always be some trade-offs in these principles and it is unlikely that we will find the perfect solution when implementing any new taxes. The trick will be to design something that meets the desired objective, for example rebalancing the tax base due to the changing environment, that would result in the least unintended consequences.

In terms of a comprehensive capital gains tax, one of the key criticisms has been that it would not generate much additional tax revenue in the medium term, if it is to be on a realisation basis.

On a wealth tax, while it might generate additional revenue on a more immediate basis, the key concern is that those individuals may leave New Zealand, which would undermine the objective of raising additional revenue and potentially result in other unintended consequences, such as capital leaving New Zealand.

If any new taxes were to be introduced, it is critical that care is taken to develop the design of them to ensure they do in fact deliver on the desired objectives in the most efficient manner. Consideration could also be given towards “recycling” tax revenue from new taxes to reduce rates or thresholds for existing taxes (e.g. personal tax cuts or bracket adjustments - the 2019 TWG considered various revenue-reducing packages in combination with proposed extensions to taxing capital gains). This could allow the efficiency and equity benefits of broadening the tax base to be realised without raising the overall level of tax collected by the Government.

Balancing these competing considerations will take time, which may be challenging if it is to be introduced as part of the Budget process (as evidenced by the potential wealth tax being considered by the Government as part of Budget 2023).

Growing the tax base

New taxes or higher rates of taxes involve the Government taking a bigger slice of the “pie”, but the best way of growing tax revenues is to grow the economy. Under a progressive tax system, as the economy grows, tax revenues grow faster. As such, consideration should also be given towards whether tax policy settings (and economic policy more generally) could help contribute to raising more revenue from existing tax settings by “growing the pie”. For example, Ireland has a lower tax-to-GDP ratio than New Zealand but in dollar terms collects a higher amount of revenue (while maintaining a lower level of government debt).

Inland Revenue’s Long Term Insights Briefing (LTIB) looked at the ways that the tax system impacts foreign investment and productivity. The LTIB considered the merits of various potential tax changes to lower the cost of capital and boost productivity, including:

Reducing the corporate tax rate;

Accelerated depreciation;

Indexing the tax system for inflation;

Changes to the thin capitalisation rules; and

Tax incentives for specific businesses or industries.

As with the consideration of adding new taxes, the above measures involve trade-offs in terms of adding further complexity to the tax system, potential for economic distortions, and a loss of tax revenue in the short and medium term. It is also likely that non-tax regulatory settings have a bigger impact on foreign investment and productivity in NZ (e.g. overseas investment restrictions and competition policy) than tax policy settings.

Where to from here?

Tax is something that intrinsically matters to many New Zealanders, and it is not surprising that it often features in election policies. However, it is important that the tax conversation continues outside of election cycles which will provide more time for New Zealanders to consider what they want or need from the tax system, resulting in more informed decisions.

As we look ahead to the longer term, in the absence of policy changes, tax or otherwise, there is the question of the sustainability of the current tax system. This is something that should be explored more and a discussion that we should not shy away from, including exploring what, if any, changes we might need to make to policy or expectations.