{{item.videoDuration}}

{{item.title}}

{{item.text}}

{{item.videoDuration}}

{{item.text}}

Over the past few years, businesses, communities and governments have responded to considerable change and uncertainty across the world including technological disruption, the COVID-19 pandemic, fractured geopolitics, social tension, climate change and rising inflation. These are having a significant effect on Aotearoa New Zealand, exacerbating some of our known long-term prosperity challenges.

As part of PwC New Zealand’s Building prosperity - A pathway to wellbeing for all of Aotearoa series, in this report we explore how Aotearoa New Zealand’s energy sector is critical to growing a more prosperous country. We focus on the capital and capability requirements and challenges to meet Aotearoa New Zealand’s decarbonisation goals, specifically with electricity infrastructure as a lead component of this journey.

Our commentary in this report includes insights drawn from a series of interviews with key energy sector leaders across Aotearoa New Zealand, to gather their perspectives on our country's future energy sector requirements to support our country's decarbonisation journey.

Aotearoa New Zealand’s access to world-leading renewable resources positions our energy sector well in regard to decarbonising the economy and supporting improved prosperity for all New Zealanders. Energy underpins nearly everything we do in modern society and delivering a sustainable, accessible, secure and relatively low cost green energy system will provide significant benefits for New Zealand households, businesses and government. It will also contribute to alleviating the impacts of climate change on future generations.

Globally the infrastructure investment required to decarbonise our energy systems is immense. To meet the UN Sustainable Development goals, US$31tr1 infrastructure investment is forecast to be required in the global electricity sector by 2040. Coinciding with this, we are in the midst of a global energy crisis, caused by the ongoing conflict in Ukraine. Nations are mobilising to meet the decarbonisation investment challenge, but how high energy costs and supply disruption will impact the speed of decarbonisation is unknown.

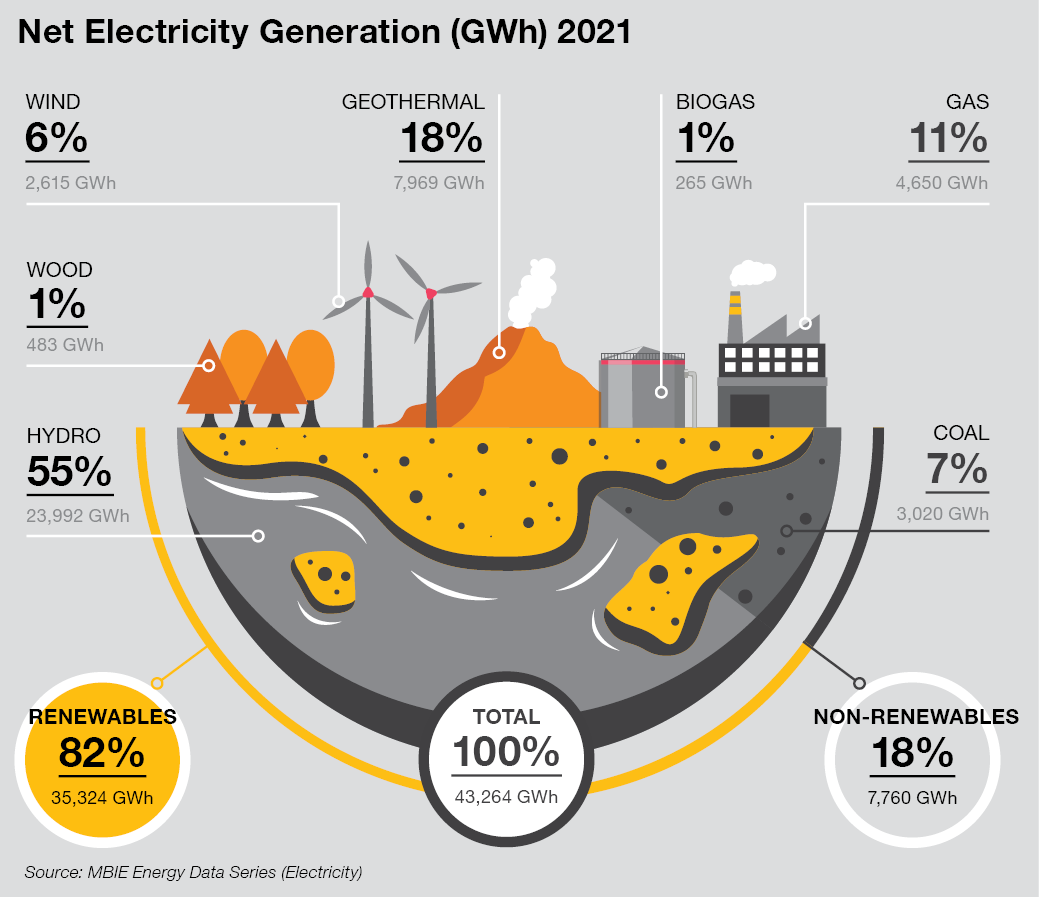

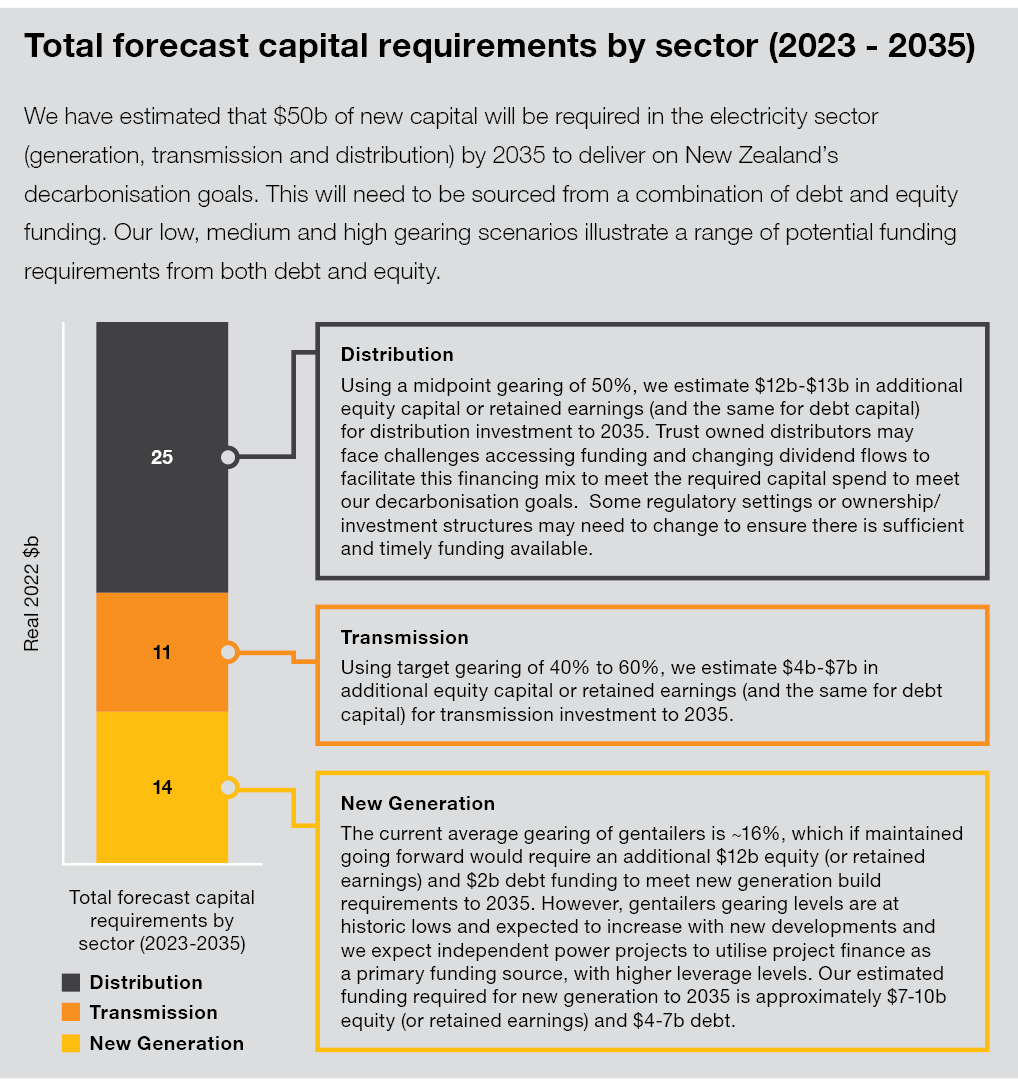

In Aotearoa New Zealand we have been relatively insulated from the global energy crisis. However, we still face a large infrastructure investment hurdle to reach our decarbonisation goals. We forecast the New Zealand electricity sector alone will require more than $50b spent on electricity infrastructure by 2035 to aid in decarbonising Aotearoa New Zealand, with the equivalent, or more, required in the following 15 years. This investment will not only enable New Zealand to transition from 82.1% to 98% renewable generation, but will also significantly reduce energy sector emissions and provide for the electrification of a large portion of New Zealand’s vehicle fleet.

In this report we focus on two themes from our Building prosperity - A pathway to wellbeing for all of Aotearoa report, being the capital and capability requirements and challenges to meet New Zealand’s energy goals, focusing on electricity infrastructure as a lead enabler of New Zealand’s decarbonisation. The energy transition will bring significant opportunity and benefits to New Zealand’s economy and both our urban and rural communities.

We need to take a whole of energy sector approach to the low carbon transition and not just focus on individual energy sector components. To decarbonise our economy we need to consider security of supply and the transmission & network investment alongside the additional renewable generation required to facilitate this change;

The global energy crisis has shown the risk of over-reliance on foreign resources. We need to create a resilient energy future for NZ that captures the benefits of international trade without putting our economy at risk;

Rising household costs are having wider societal impacts in New Zealand and we need to ensure the energy transition does not exacerbate these. We must consider equity between those who can afford to transition early, vs those that cannot.

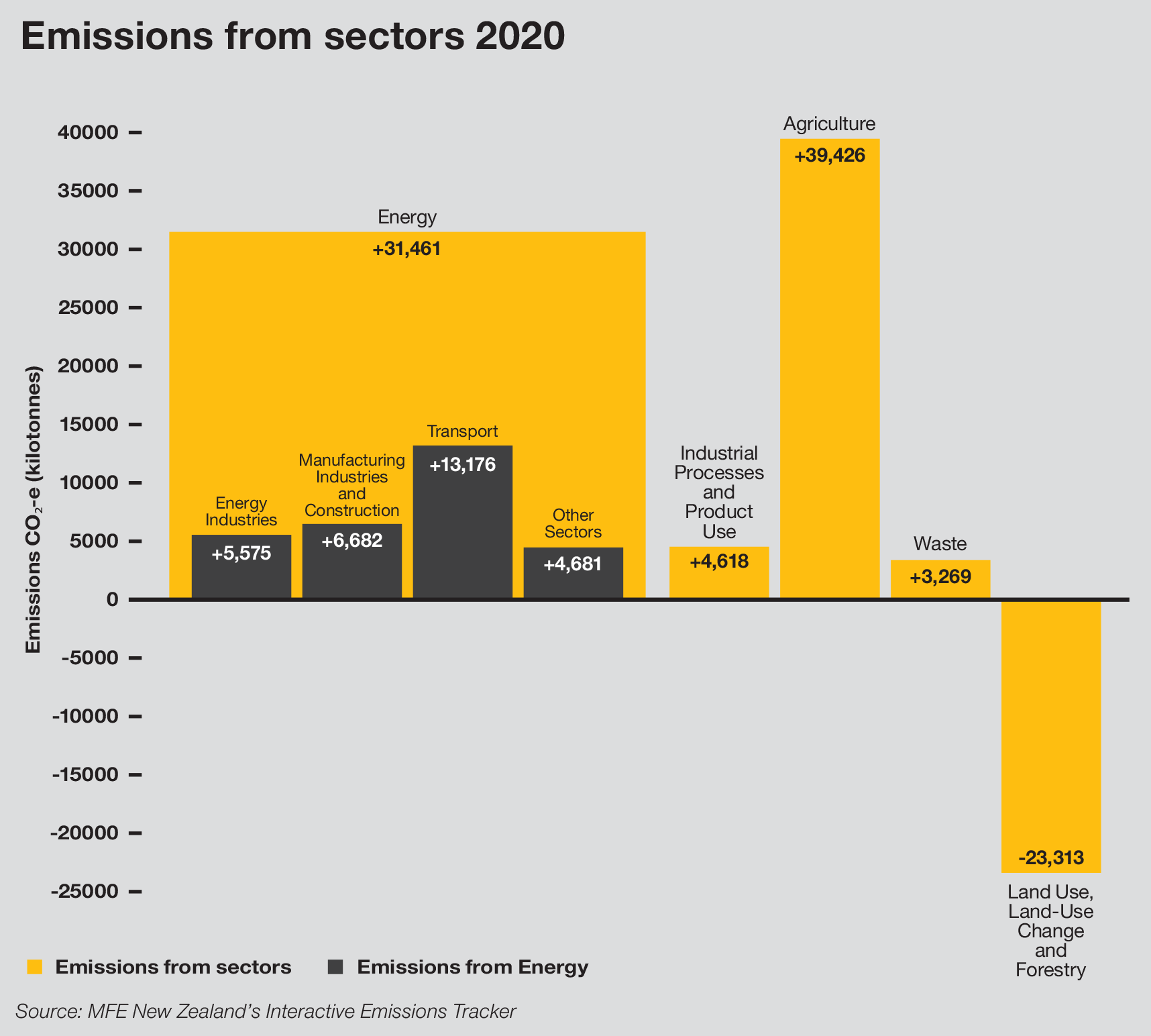

In this paper we focus on electrification, which is expected to be the sector’s largest lever for decarbonisation. However, we acknowledge we cannot build a future energy system without considering the future molecule-based components of our new energy system. As a nation we will also need significant focus and investment in new green alternate fuels to support decarbonisation of those areas more difficult (or costly) to electrify.

The opportunity for New Zealand to electrify its energy system and provide potentially low-cost (relative) green energy for all New Zealanders is real, and has been documented in many reports and forecasts on the sector. However, the challenge of executing this goal is significant. If we are to deliver change efficiently, on-time and in a manner that engages all New Zealanders, key barriers and challenges for the sector need to be addressed early. As mentioned earlier, two areas we see as critical to success in executing our low carbon transition, and lifting prosperity for all of Aotearoa New Zealand include:

rethinking capital allocation and overseas investment; and

creating a future fit workforce

Aotearoa New Zealand is seen as a safe haven for energy investment. Our energy system has been relatively insulated from global shocks and our high renewable generation levels (82% in 2021) and clear intention to decarbonise the economy provide comfort for international investors. Additionally we have stable regulation frameworks and little intervention/subsidies in our markets, providing a strong base for investor confidence.

To date we have seen strong capital markets support for investment and growth in the sector. While this has predominantly been through existing players (e.g. gentailers or transmission/distribution companies) there is growing interest from new entrants in independent generation opportunities. This is providing opportunities for increased local and regional participation in renewable electricity sources, given the diversity in the scale and location of potential plants.

Looking forward, large capital requirements for decarbonisation are an opportunity for New Zealand to increase the diversification of both local and international capital into the energy sector. Renewable energy and transmission/distribution investment will have a large regional component, providing opportunities for local, Iwi and other community involvement, in deployment, maintenance and potentially investment in these assets. We also expect continued offshore support debt and equity markets support for the sector - particularly if we can maintain our largely stable and low intervention environment.

Supporting regional investment in the sector: Renewable generation and network/transmission infrastructure provide an opportunity for direct investment into regional New Zealand. As well as the regional economic benefits these developments will bring, investment or co-investment opportunities for local communities, trusts and businesses should be considered, to allow communities to play an active role in their decarbonisation and provide investment for future generations to benefit from.

Ensuring we have access to capital where needed, or new funding models for those areas that cannot readily access capital: Components of the energy sector, particularly trust owned electricity networks, may face challenges accessing funding or changing dividend flows to facilitate the required capital spend to meet our decarbonisation goals. Ongoing engagement between networks, trusts and trust beneficiaries will be required to ensure sufficient capital is available to meet the investment needs in our future electricity system. Engagement with large customers increasing load due to electrification initiatives will also be important in planning future capital needs and accessing targeting funding such as EECA’s GIDI fund.

Facilitating a smooth transition for any Resource Management Act (RMA) changes: This reform may, in the short and medium term, create a transitional period of uncertainty and learning while the legislation is enacted and consenting authorities adapt to the new regime. To manage this, rollover and grandfathering provisions will be likely. Nonetheless, these material changes to the RMA legislation will be central to successful project execution and it will be important for transitional impacts to be mitigated, if possible, during this critical phase in Aotearoa New Zealand’s decarbonisation journey.

Attracting green capital: ESG and green investment categories are growing rapidly worldwide and will be important contributors to Aotearoa New Zealand’s decarbonisation. Recent PwC global research outlined several priorities to attract private green capital, which included clear and comprehensive net zero plans, greater collaboration across sectors and value chains, a financial market focus on emissions when lending and investing, heavy investment and taxpayer support for emerging decarbonisation technologies, and clear price signals through carbon prices or taxes. Aotearoa New Zealand has progressed many of these, and finalisation of our national Energy Strategy3 and maintaining stable policy and regulatory settings will be important to continue to attract these investors.

Partnering with Māori for mutual value: The energy sector plays a critical role within Māori culture due to its use of and affinity to natural resources. Energy is also a key input to production in many industries where Māori feature strongly, e.g. fisheries and agriculture. As a partner to Te Tiriti o Waitangi, Māori have an important role in New Zealand’s decarbonisation journey, to both support policy changes and also to be direct investment partners. Where Māori have partnered and invested in energy there have been significant economic and synergistic benefits for all New Zealanders.

Review of regulation to facilitate early transmission and network build: New Zealand’s current “just in time” regulation for development of new transmission and distribution spend has served us well in the past for spend efficiency, but going forward will likely constrain renewable growth. Additionally, just in time approvals will restrict the ability to develop long term capital plans and supporting contractor workforce capacity to service a portfolio of major developments. Adjusting these settings to allow for early and increasing spend, increasing flexibility in the regulatory settings to adapt to large unforeseen capex, and streamlining regulatory approvals will all assist with executing elevated levels of grid and network investment. The regulatory settings must consider the financeability of the network programmes which are being approved.

Stimulating innovation capital into the sector: Considering how Aotearoa New Zealand promotes and accesses innovative capital into the sector will be important, particularly as smart energy systems and responsive demand become an increasing part of our electricity system. Investment into these new technologies will typically come from alternative sources to traditional infrastructure capital, but will be an important capital component for developing an efficient and effective future electricity system. For example:

Intelligent asset management and the use of data and analytics tools will aid in optimising asset investment;

Distributed energy resource balancing and trading will offset the need to upgrade network capacity or invest in peaking generation; and

Automated systems will allow smart devices to automatically manage domestic energy demand reducing grid capacity needs.

Developing New Zealand’s market for long-term power purchase agreements (PPAs): Long Term PPAs are a key component to support the growth of independent power producer projects and financing. Developing and growing PPA markets will help New Zealand competitively access both new equity and debt capital for renewable electricity developments.

Aotearoa New Zealand’s new generation and transmission/distribution investment will require a significant increase in people and local delivery capability. New Zealand's current electricity sector workforce is estimated at 8,000 across generation, transmission, distribution, retail, and contract service providers4. We forecast an increase in the required distribution and transmission sector workforce of between 45% - 75% by 2035 to deliver the additional investment. To meet this, we need to consider how to strategically develop and attract this talent, both within New Zealand and from offshore. New Zealand will be competing with global demands for energy sector talent as the world invests trillions in energy infrastructure to decarbonise our economies.

Increasing the workforce within Aotearoa New Zealand will require significantly more training capacity. It will also require New Zealand consideration of how we can transition more people into the industry at later stages of their career. Without doing so, we will be reliant on attracting skilled people from overseas to fill this gap, which will be challenging given global demands for this talent.

Increasing the capacity within the sector also presents an opportunity to increase diversity at the same time. Women, Māori and Pacific peoples are currently underrepresented in the sector. In 2020, it was reported that nearly twice as many men than women were employed in the electricity sector in New Zealand5.

As well as building sector capability it will be important to consider how we enable efficient delivery models. The increasing quality and resilience required of electricity infrastructure, adds complexity to projects. With construction skills at a premium we need to consider whether we have the right price/quality tradeoff in what we build, to ensure an efficient level of capital spend and resourcing in the sector.

The opportunity to attract a more diverse workforce. As part of building the future energy sector workforce, a focus should be placed on increasing diversity, especially with Māori, Pacific peoples and women. This will be essential to building capability and capacity, as well as bringing benefits of diverse backgrounds and perspectives to the sector. Contact Energy’s Māori intern programme and the partnership between Southland Girls’ High School and NZAS to encourage female students to pursue careers within the engineering and science fields are examples of initiatives already underway in this area, but many more are needed.

Increasing both central and regional training for the sector: Building skills at both national and regional levels will be required to build the future energy sector workforce. Regional vocational training facilities working in partnership with local networks, community trusts, schools and local iwi could contribute significantly to this task.

Greater use of partnerships to bring international best practice and capabilities into New Zealand: Smart delivery of investment will be critical to reaching our renewable electrification targets. As the global energy system is on a similar decarbonisation journey to Aotearoa New Zealand, there are opportunities to access smarter ways of doing things by partnering with industry leaders to bring leading approaches and capabilities to Aotearoa New Zealand e.g. Solar partnerships. Additionally, as work practices, equipment and technology continue to evolve across the globe, we need to be looking for innovative solutions which can be deployed here to assist our workforce to deliver more efficiently. For example, enhanced works management and field force automation can improve productivity.

Greater promotion of the sector as an attractive employment option. This could involve enhancing and promoting skills pathways for young people at the time they enter the workforce, or re-enter the workforce, to attract people who may have traditionally worked in other sectors. Promoting the sector as having good employment opportunities and assisting in decarbonisation across regional Aotearoa New Zealand will also help attract those wanting to live and work outside the main centres.

Greater coordination across industry participants in bundling major work programmes to enable large contractors to develop local capability and capacity: To attract and grow the large scale contractors to deliver our new energy infrastructure, cross industry efforts are needed to demonstrate the pipeline of significant works. This will ensure large scale contractors have the confidence in work programmes to respond and invest in appropriate capability and capacity in New Zealand. Increasing workforce utilisation through these programmes of work will also help to deliver the scale of work required. Additionally given the disaggregated nature of the distribution sector, more collaboration between networks to combine work programmes and engage larger contractors to deliver them on a regional basis will help improve regional capabilities, workforce capacity and delivery of capital investment.

Reconsider our immigration settings to attract talent from across the globe, not only from traditional markets, and remove barriers for sector talent: Ensuring the settings are targeted to the specific needs of the energy sector including electrical engineers, technicians, linesmen, cable layers and project managers will help the workforce growth challenge. Coordination will be required at a sector level however, to ensure we grow the right and sufficient talent for the industry as a whole, not just the individual organisations.

In this paper we have explored two areas which can support the decarbonisation of our energy system and Aotearoa New Zealand, helping to lift prosperity through providing potentially low-cost (relative) green energy for all New Zealanders. These two areas are:

- rethinking capital allocation and overseas investment; and

- creating a future-fit workforce

We also recognise there are many more opportunities and challenges that sit outside of those areas explored in this paper to enable a more prosperous Aotearoa New Zealand. This includes the need for greater joined up thinking across New Zealand’s decarbonisation journey and consideration of the potential societal impacts the energy transition will bring, and what the energy sector can do to alleviate these, especially in the current environment of rising inflation and cost of living.

Getting the energy transition right is a significant opportunity for New Zealand. The returns for our nation in getting it right are large and could mean affordable, secure and green energy for all of Aotearoa New Zealand. To achieve this we must act now to facilitate the capital and capability required to deliver our future low carbon energy sector and economy.

We’d like to thank all the energy leaders we interviewed as part of developing this report who candidly provided their perspectives on the opportunities and challenges, as the sector supports Aotearoa New Zealand’s decarbonisation journey.

Our community of solvers help our clients to build trust and deliver sustained outcomes for their stakeholders, communities and people as they navigate the energy transition. As one of the world's leading advisors to the energy industry, we work with every segment of the market, drawing on our experienced industry leaders across New Zealand and the global PwC network, to provide business solutions tailored to your needs.

In New Zealand, we work for generators, transmission and distribution networks, retailers and government delivering solutions tailored to our clients’ or country’s needs. We bring specific experience on a range of regulatory, commercial, transaction, funding, technology, risk, operational transformation and strategy matters. Building our future energy system will require national, regional and individual organisation efforts, and at PwC we are committed to helping New Zealand succeed in this journey.

1 https://outlook.gihub.org/?utm

2 Year to December 2021. Source: https://www.mbie.govt.nz/assets/Data-Files/Energy/nz-energy-quarterly-and-energy-in-nz/electricity.xlsx

3 MBiE: New Zealand Energy Strategy

4 The future is electric, BCG 2022

5 Mind the Gender Gap: Energy Employment Trends in Aotearoa New Zealand, The University of Auckland

{{item.text}}

{{item.text}}

Brett Johanson

A definition of Social Cohesion

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum.